Prediction finance (let’s call it PreFi) is the use of prediction market positions as collateral for DeFi lending. It’s attracted real attention from serious teams, like Kalshi and Solana, Gondor, and Polymarket. What it hasn't attracted yet is meaningful TVL. This post explains why, and walks through the pricing approaches most likely to change that.

PreFi allows prediction market positions to be used as collateral in DeFi lending protocols, the same way ETH or USDC is used today. A user holds a $1,000 position in a Polymarket or Kalshi event, posts it as collateral, and borrows against it.

One of the advantages of onchain finance is that it can be composable in this way. Liquid staking tokens and RWA looping are just two examples. Blockchain oracles are critical components, enabling a kind of dynamic composability that’s not seen in traditional finance.

PreFi seeks to integrate prediction markets into this world of DeFi composability. The idea is straightforward. Executing it safely is not.

Many DeFi lending protocols use a midpoint price, the average of the best bid and best ask from several exchanges, to value collateral. This works well for liquid assets like ETH because:

When a protocol needs to liquidate ETH collateral, it can sell at close to the quoted price. Risk is manageable.

Prediction markets are thin relative to blue-chip crypto. Total liquidity across Polymarket, Kalshi, and similar platforms runs in the low tens of billions, versus hundreds of billions for major crypto markets. More importantly, that liquidity is spread across hundreds of thousands of active events, most of which see very little trading activity.

Thin markets create two problems for PreFi that midpoint pricing cannot solve:

Prediction market liquidity as a whole is still below the thresholds that would make DeFi lending protocols comfortable using positions as collateral, which leads to slow uptake and large haircuts.

Active PreFi efforts tend to fall into one of two categories: experimental (no real capital at risk) or live with large haircuts. Gondor, one of the few protocols with markets live, applies a 50% haircut, meaning $100 of prediction market positions supports only $50 in borrowing capacity. That protects the protocol but makes the product less attractive to borrowers.

The question is whether better pricing can close that gap.

The following approaches represent real paths forward for DeFi prediction market lending. All can be thought of as attempts to estimate price impact of a liquidation trade and manage risk accordingly. None is perfect. Each involves tradeoffs between lender protection, borrower incentives, and manipulation resistance.

Instead of the midpoint, this approach uses the best bid as the collateral price. Since a liquidation is a sell, the best bid is the highest price actually achievable at that moment.

This is a marginal improvement. The best bid yields a more accurate price estimate than the midpoint in thin markets, but it shares the same fundamental weaknesses: it doesn't account for slippage on large positions, and it's just as easy to manipulate. Anyone who can move the midpoint can move the best bid.

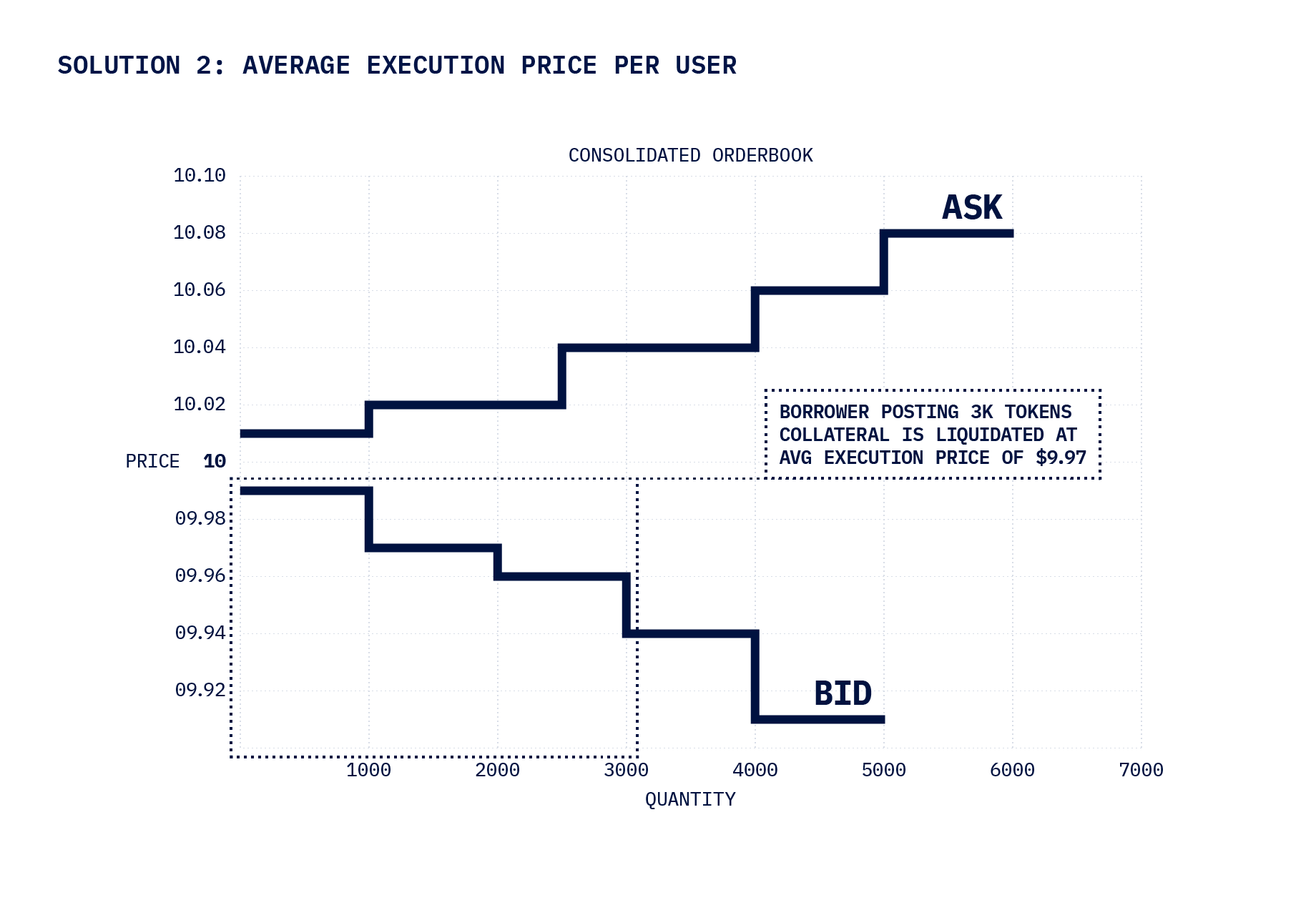

Rather than using a single price point, this approach models the actual sell sequence. It walks down the order book bid by bid, hypothetically filling the full position size, and computes the weighted average execution price. If a $10,000 position fills $2,000 at the best bid, $3,000 at the next level, and $5,000 at the level below, the weighted average is the collateral price.

This approach accounts for slippage directly. There are no surprises at liquidation because the protocol has already priced in the market impact. The downside: larger positions get penalized more heavily. A user with a $100,000 position faces a much lower collateral value than a user with a $1,000 position in the same market. That is accurate from a risk perspective, but it deters larger borrowers.

This approach groups all users in a market into bands by position size. For example, the smallest 10% of total open interest, then the next 20%, then 30%, then the largest 40%. Each band gets its own liquidation price, calculated as if the entire band were liquidated simultaneously.

The advantage of banding is that it reduces correlation between liquidation events. By designing bands with meaningfully different liquidation prices, a protocol reduces the likelihood of triggering cascading liquidations. Smaller positions benefit from landing in lower-slippage bands. Larger positions get some collective risk benefit.

The remaining weakness: this model is still vulnerable to manipulation. A coordinated actor can move prices regardless of how positions are banded.

Adding a time-weighted average (TWAP) to any of the above approaches provides a meaningful defense against manipulation. The key insight is that price manipulators minimize their market exposure: they spike the price briefly and exit. A TWAP smooths short-lived spikes, making manipulation more expensive relative to the potential benefit.

.png)

The tradeoff: TWAP introduces lag. A rapidly falling market moves the TWAP more slowly than spot, which means the protocol is slightly behind on risk in fast-moving conditions. Liquidation probability is modestly higher overall. The protection against gaming is substantially better.

No single solution works for every protocol. The right choice depends on the specific risk profile: how much manipulation resistance matters, how important it is to support large positions, and how much liquidation probability the protocol can tolerate.

These pricing approaches are not theoretical. They are implementable today, but only with oracle infrastructure built to support them.

Simple midpoint prices updated every few minutes are not sufficient for any of the solutions above. Order book depth data, sub-second latency, and TWAP feeds computed at useful frequencies are all necessary inputs.

Stork price feeds are built for the latency and data granularity these approaches require. On a typical day, Stork feeds power more than half the volume in onchain perpetuals trading. Stork can have new feeds live within minutes of an asset's TGE, and has powered equity perpetuals pricing solutions that cut across times of market transition with consistency and risk management. Flexible underlying oracle architecture built to meet these demands enables Stork to quickly develop other solutions, including the pricing approaches for PreFi, described above.

For any team evaluating DeFi prediction market lending architecture, oracle selection is not a secondary consideration. It determines what is possible in the market.

The prediction finance space is early. TVL is thin. But as in other areas of onchain finance, creative pricing solutions can give teams an edge in go-to-market with new products.

If you are evaluating oracle infrastructure for a prediction finance or DeFi prediction market lending protocol, or any innovative use case, contact Stork or reach out at @StorkOracle.