When a trader takes a position in an equity perpetual on a decentralized exchange, they are not buying a share of stock. The position is a contract whose value is derived entirely from data, such as a price feed provided by a blockchain oracle. No shares change hands, and no custodian holds anything on anyone's behalf.

This is distinct from most tokenized stocks, where issuers hold shares in a brokerage account, or stablecoins like USDC, where a dollar (or dollar equivalent) sits in a bank account. With tokenization, the token is the receipt for an equity share or a dollar.

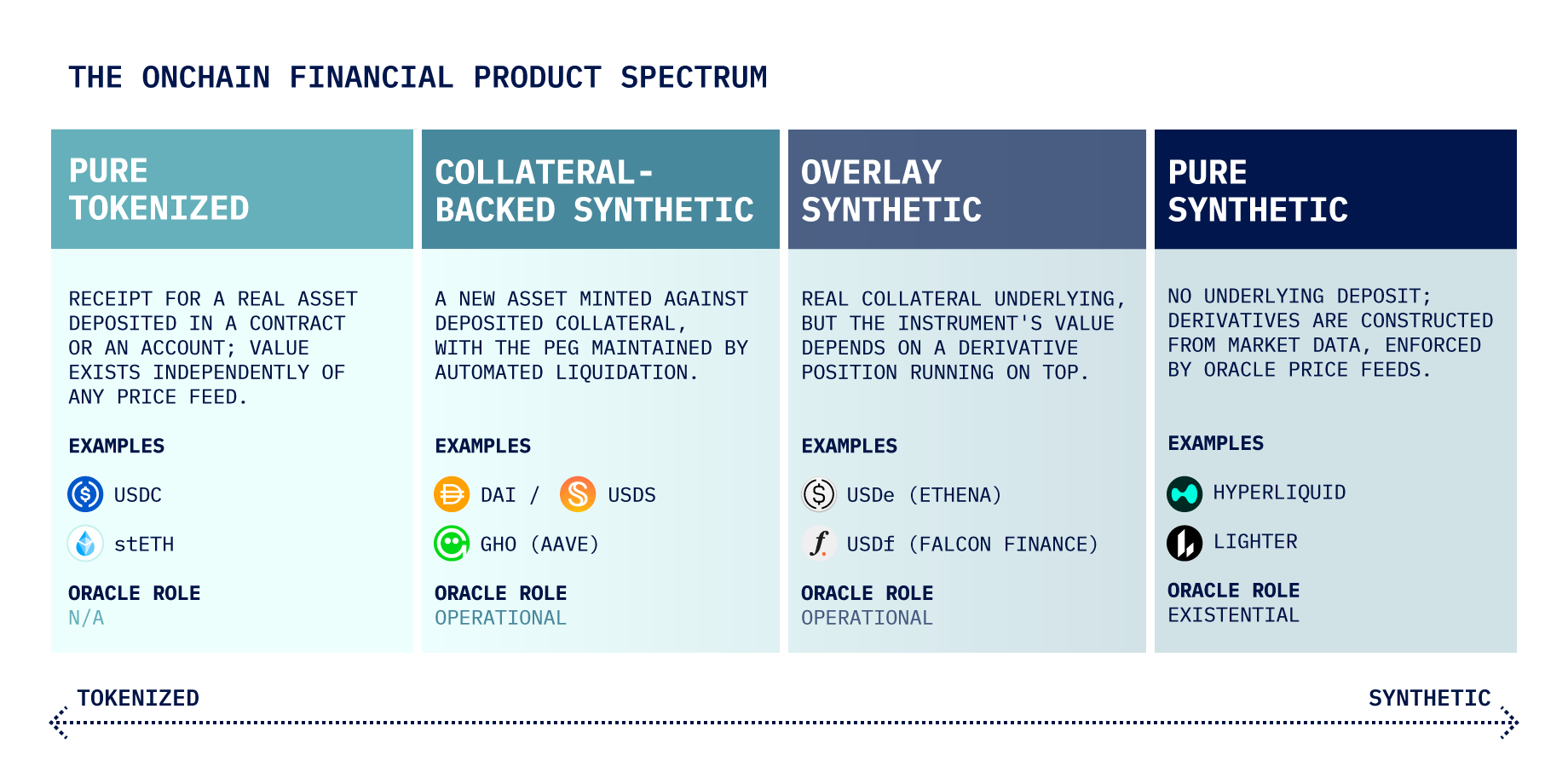

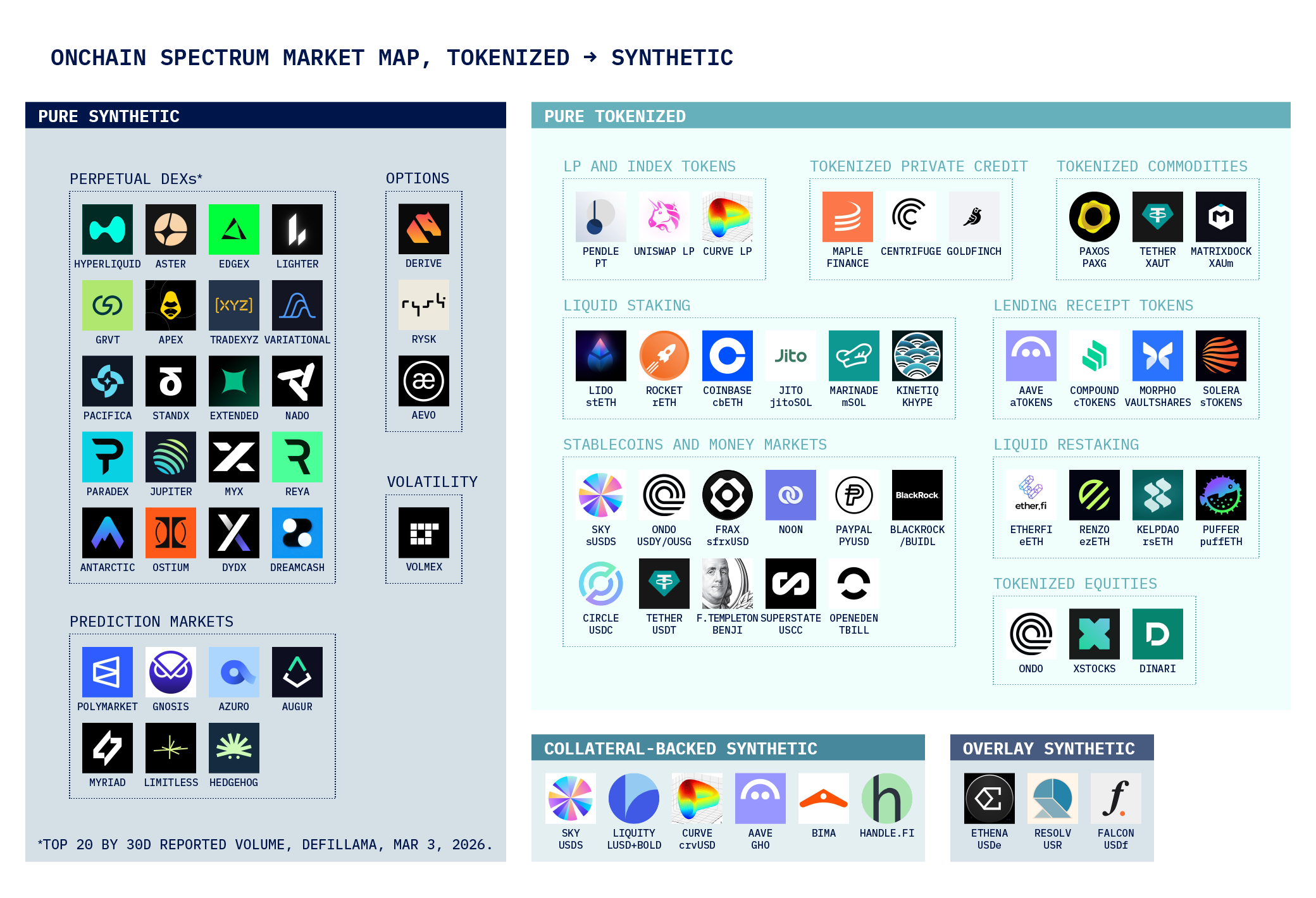

This distinction exists in all areas of finance, but crypto has a middle ground, forming a spectrum between synthetic and physical that traverses some of the most fascinating territory in finance today.

Equity perps and tokenized stocks represent opposite ends of a spectrum: on one end, deposits determine value. On the other, it’s market data, primarily oracles.

Understanding where new assets and asset categories might fit on this spectrum is useful for investors trying to measure risk and for builders working to innovate in onchain finance. Where an asset sits in this framework tells you something about its risk profile, its dependence on external data, and its potential to combine with other products to create new instruments. The spectrum is highly applicable to real-world assets (RWAs), but also includes crypto-native products.

The core distinction is straightforward. A tokenized product is a claim on a deposit. When you hold a tokenized T-bill, redemption produces a real asset. When you hold a synthetic derivative like a perpetual position, its value is whatever the price feed says at that moment. There is no underlying asset to fall back on, because you never owned one. It’s one reason why oracle reliability is so important for perp DEXs.

This article maps onchain financial assets using four categories, including two that are in the middle, between tokenized assets and synthetics.

Each category carries a different risk profile and a different relationship to the data infrastructure that underpins it.

A pure synthetic has no deposit behind it. The asset’s value depends entirely on data. If the oracle stops reporting, the position has no value to fall back on, making oracle reliability not an operational concern but an existential one. The most familiar examples are perpetual futures on decentralized exchanges, onchain options, and prediction market contracts.

The existential data dependency also shapes what asset classes are feasible as pure synthetics. Equity perps, for example, require a feed that reflects the price of a stock trading on a regulated exchange with defined market hours, corporate actions, and potential trading halts. A blockchain oracle must handle all of that accurately and in real time, because there is no underlying holding to anchor the position if the feed diverges from reality.

Representative products include perpetual DEXs such as Hyperliquid, Lighter, and dYdX; and onchain options protocols such as Aevo, Derive, and Rysk. Each requires a continuous, reliable price feed. Prediction market platforms such as Polymarket require oracle data to resolve markets. The growth of this category has expanded access to asset classes like equities into 24-hour and cross-border venues.

An overlay synthetic holds real collateral but constructs the instrument's value through a derivative position running alongside that collateral. The clearest example is Ethena's USDe. The protocol holds crypto assets as collateral and simultaneously runs a short perpetual position on a derivatives exchange. The short cancels out the price exposure of the collateral, leaving a position that holds its dollar value through a derivative overlay rather than a dollar deposit. Blockchain oracles play an important operational role in each component, alongside the existence of a verifiable deposit.

A useful analogy from traditional finance is the currency-hedged equity ETF. Such a fund holds foreign stocks as real assets and overlays a currency forward to neutralize FX exposure. The fund's return comes from the underlying equities; the hedge removes one dimension of risk. In Ethena's case, the underlying is crypto collateral and the hedge removes price risk, leaving the funding rate as the yield source. In both cases, the collateral is real, but the instrument is constructed using oracle data.

The important distinction from a collateral-backed synthetic (discussed below) is what happens when the overlay fails. In a CDP like DAI, falling collateral value triggers liquidation, and the system can self-correct given sufficient collateral and timely execution. In Ethena, persistent negative funding rates turn the yield into a loss, and the peg comes under pressure even though the underlying collateral still exists. The risk sits in the derivative position, not in the assets backing it.

A collateral-backed synthetic mints a new asset against locked collateral. The minted asset does not represent the collateral; it is a new instrument whose peg is maintained through the threat of liquidation. Liquidation is managed via price feeds from a blockchain oracle: if collateral value falls below a threshold, the protocol automatically sells the collateral to cancel the outstanding synthetic. The depositor absorbs the loss, and the synthetic's peg is preserved.

The framing from traditional finance is a secured loan with margin calls. A borrower pledges collateral, receives a new asset, and faces forced liquidation if the collateral falls in value. The key difference onchain is that the liquidation process is automatic. Smart contracts can execute it when oracle-supported price feeds cross the threshold, with no intermediary involved.

Representative protocols include Sky (formerly MakerDAO), which issues USDS against crypto collateral; Liquity, which issues LUSD against ETH with no governance and no stability fees; and Curve, whose crvUSD uses a soft-liquidation mechanism that converts collateral gradually rather than in a single event. These protocols have operated across multiple market cycles and represent some of the most tested infrastructure in onchain finance.

A pure tokenized product is a receipt for something on deposit somewhere, whether in a smart contract onchain, a bank account, or a brokerage account. The token's value is not constructed from data; it is a claim that can be redeemed for the underlying asset. A blockchain oracle may be useful in a variety of ways connected to tokenized assets, but the asset does not derive its value from data. If the oracle goes down, the token still has value, because the underlying asset still exists.

The category is broad. Firms like Ondo’s AAPLon and xStocks’ xAAPL are tokenized representations of Apple stock, among many tokenized equities these firms issue. Stablecoins like USDC and USDT are claims on dollars and cash equivalents in bank accounts. Liquid staking tokens like stETH are claims on staked ETH plus accrued rewards. Tokenized T-bills like BUIDL and OUSG are claims on U.S. government securities. Gold tokens like PAXG are backed by physical gold in vaults. Receipt tokens from lending protocols like Aave are claims on deposited assets plus interest. In each case, a deposit is held, and the token is the claim on it, whatever any oracle may indicate.

When you consider these products alongside purely synthetic equity perps, the spectrum of risk and composability in onchain finance comes into view.

The examples in this framework point toward composability as one of the most consequential properties of onchain finance. In traditional markets, combining products from different institutions requires legal agreements, reconciliation between separate ledgers, and operational overhead. That friction limits how quickly new structures can be assembled and how granular they can be. On a shared ledger with fast finality, the cost of combining two products falls dramatically. This is not just a technical improvement; it changes what is economically viable to build.

Blockchain oracles are the mechanism that makes composability work across product categories. A tokenized T-bill needs a price feed to serve as collateral in a lending protocol. A delta-neutral yield product needs a reliable rate index. An equity perp needs a price feed fast enough to support active position management. In each case, the oracle is not background infrastructure. It is the component that allows one product to interact with another. The failure mode of a bad oracle in a composed system is systemic.

Stork has operated as a blockchain oracle with five-nines availability for longer than any other perp DEX oracle. Its architecture is built for speed and flexibility. For protocols building at the intersection of the product categories described in this framework, we view reliability as the infrastructure condition that makes dynamic composability possible.